When a fund manager has a directional view on a stock (bullish or bearish), the most obvious tools are buying a call or buying a put. But standalone options can be expensive, and the full premium is lost if the stock does not move enough. Spreads solve this problem.

A spread is built by buying one option and simultaneously selling another option of the same underlying, same expiry, but at a different strike price. The premium collected from the sold option reduces the net cost of the bought option. In exchange, the maximum gain is capped at the sold option's strike.

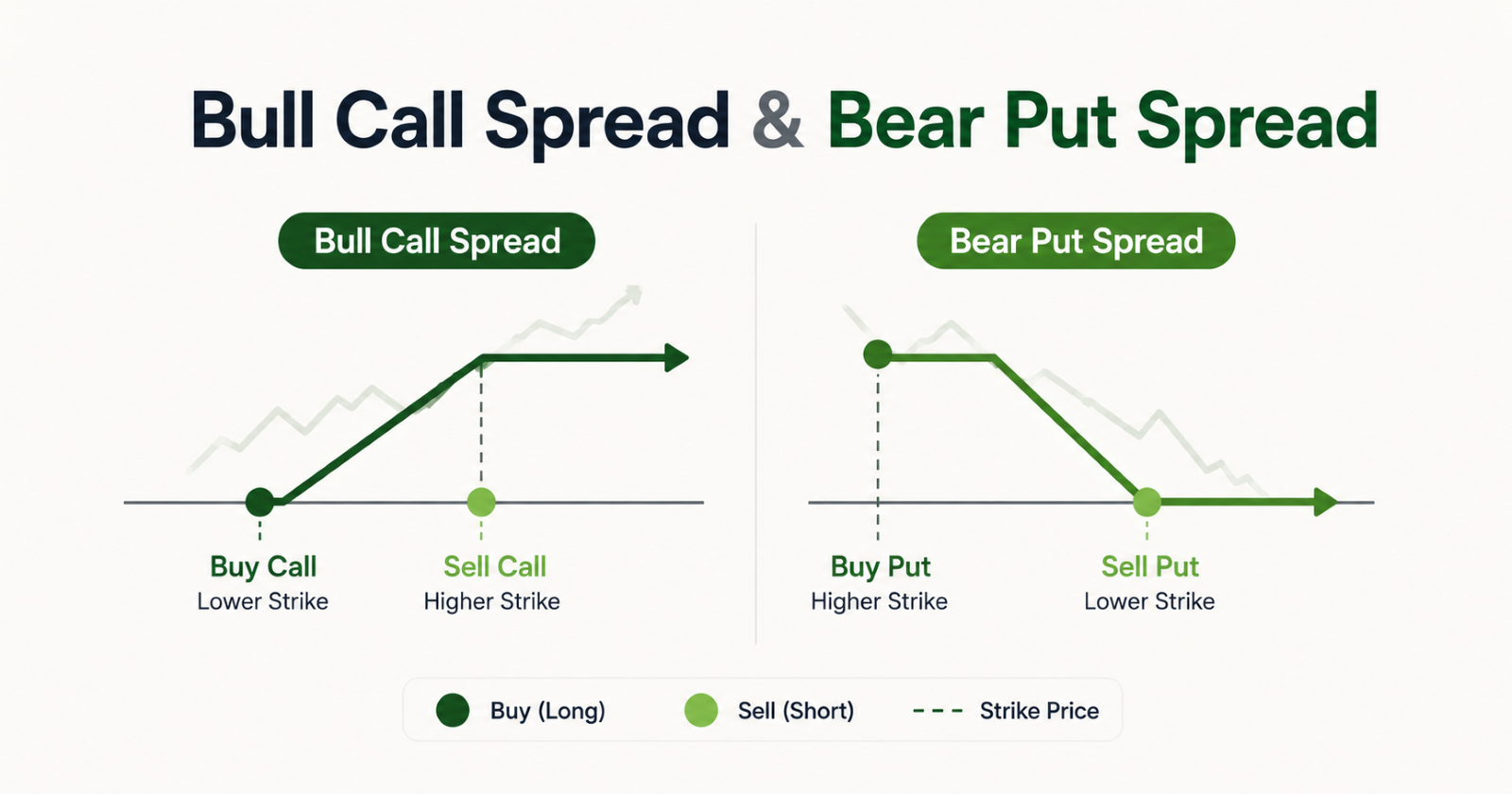

Long vs Short

Bull Call Spread | Bear Put Spread | |

View | Moderately Bullish | Moderately Bearish |

Built by | Buy lower strike call + Sell higher strike call | Buy higher strike put + Sell lower strike put |

Profit when | Stock rises toward or above higher strike | Stock falls toward or below lower strike |

Loss when | Stock stays flat or falls | Stock stays flat or rises |

Max gain | Spread width minus net premium paid | Spread width minus net premium paid |

Max loss | Net premium paid | Net premium paid |

When Does an SIF Manager Use This?

Bull Call Spread: Used when the manager has a moderately bullish view on a stock with a specific upside target. Instead of buying a plain call, which costs more and requires the stock to keep rising beyond the premium, the manager buys a call at a lower strike and simultaneously sells a call at the target price. The sold call funds a significant portion of the bought call's premium.

Bear Put Spread: The mirror strategy for a moderately bearish view. The manager buys a put at a higher strike, and sells a put at the expected downside target. The sold put at the lower strike funds a significant portion of the bought put's cost.

In the SIF context, spreads are exposure-efficient tools. Per the SEBI circular, options bought are counted in gross exposure based on premium paid. Options sold are counted at full notional value = Market Price of Underlying × Lot Size × Number of Contracts. In a spread, the sold option partially offsets the gross exposure of the overall position compared to running two standalone legs. This makes spreads a capital-efficient way to express directional views within the SIF's overall gross exposure limit of 100% of net assets.

How It Plays Out

Bull Call Spread Setup: Stock A trading at ₹2,500. Manager buys a call at strike ₹2,500 (premium ₹120 per share) and sells a call at strike ₹2,700 (premium ₹60 per share). Net premium paid = ₹60 per share. Lot size 500. Net cost = ₹30,000 per spread.

Scenario | Long Call (₹2,500 strike) | Short Call (₹2,700 strike) | Net Impact |

Stock rises to ₹3,000 | Gains ₹500/share | Loses ₹300/share | Capped gain: ₹200 − ₹60 (net premium paid) = ₹140/share |

Stock rises to ₹2,700 | Gains ₹200/share | Expires at strike | Maximum gain: ₹140/share |

Stock stays at ₹2,500 | Expires at strike | Expires worthless | Loses net premium: ₹60/share |

Stock falls to ₹2,200 | Expires worthless | Expires worthless | Loses net premium: ₹60/share |

Bear Put Spread Setup: Stock B trading at ₹1,000. Manager buys a put at strike ₹1,000 (premium ₹80 per share) and sells a put at strike ₹800 (premium ₹35 per share). Net premium paid = ₹45 per share. Lot size 400. Net cost = ₹18,000 per spread.

Scenario | Long Put (₹1,000 strike) | Short Put (₹800 strike) | Net Impact |

Stock falls to ₹600 | Gains ₹400/share | Loses ₹200/share | Capped gain: ₹200 − ₹45 = ₹155/share |

Stock falls to ₹800 | Gains ₹200/share | Expires at strike | Maximum gain: ₹155/share |

Stock stays at ₹1,000 | Expires at strike | Expires worthless | Loses net premium: ₹45/share |

Stock rises to ₹1,200 | Expires worthless | Expires worthless | Loses net premium: ₹45/share |

Two things stand out across both tables. First, the maximum loss in either spread is always just the net premium paid, which is a fraction of what a standalone long option would cost for the same directional exposure. Second, the maximum gain is always capped, no matter how far the stock moves beyond the sold strike, the profit does not grow further. That is the explicit trade-off: lower cost entry in exchange for a ceiling on the upside.