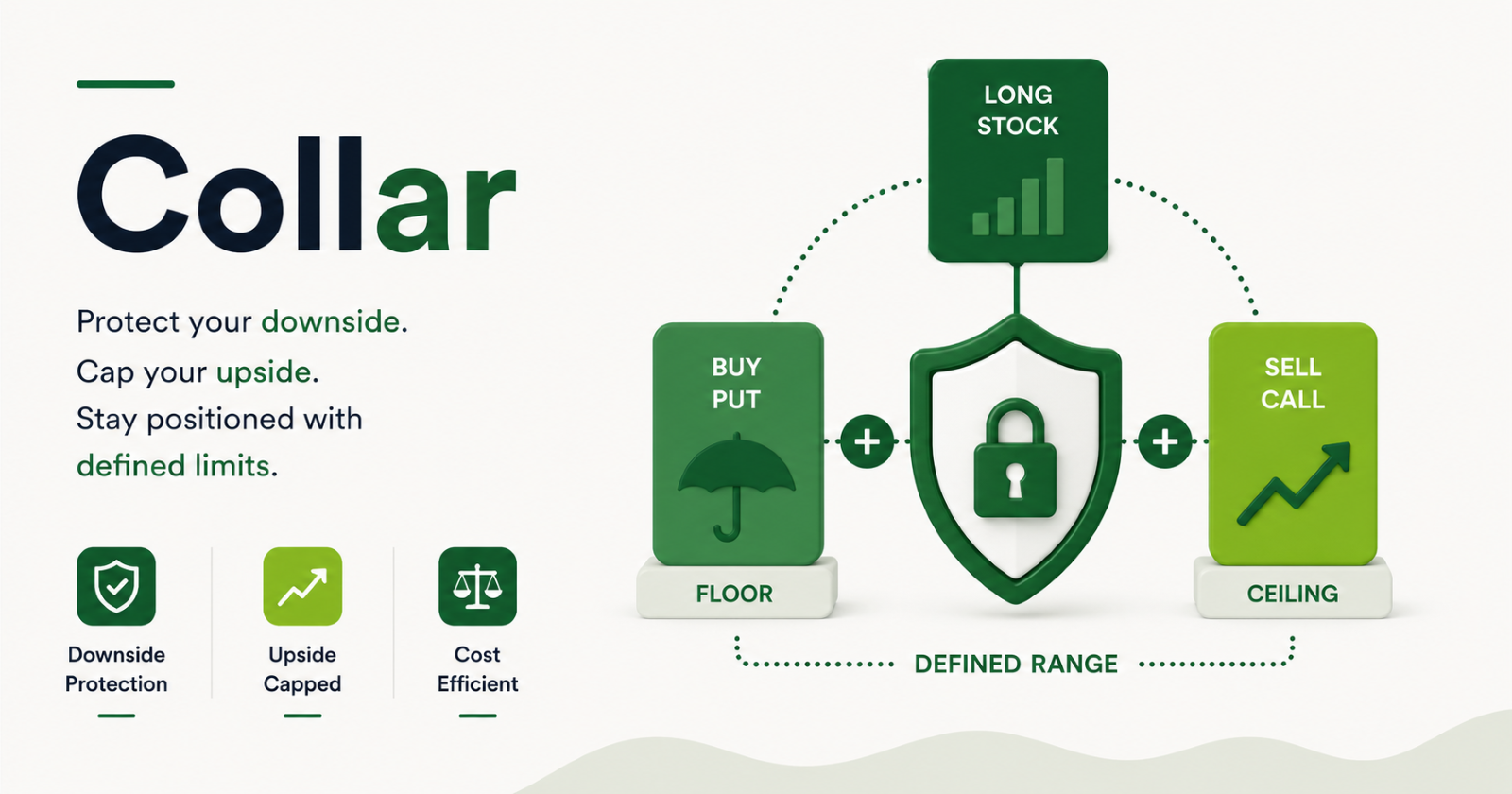

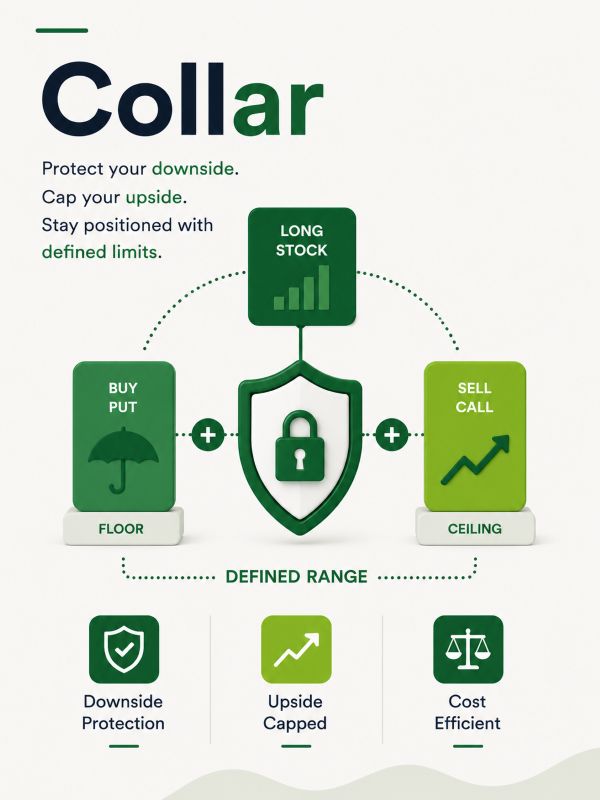

A collar combines two strategies (protective put and covered call), applied simultaneously on the same stock position.

The manager holds a stock, buys a put to protect the downside, and sells a call to fund the cost of that put. The premium collected from selling the call partially or fully offsets the premium paid for buying the put. The result is a position with a defined floor below and a defined ceiling above, the stock is "collared" between two price levels.

When Does an SIF Manager Use This?

A manager uses a collar when they want to hold a stock through a period of significant uncertainty, but cannot afford the full premium cost of a standalone protective put.

The covered call finances the protection. The trade-off is giving up upside beyond the call strike. But if the manager's near-term view is genuinely uncertain rather than bullish, that upside sacrifice is acceptable.

In the SIF context, the collar is a hedging combination and does not consume the 25% unhedged short limit. The put is bought for protection and the call is covered by the underlying stock holding; both qualify as hedging and portfolio rebalancing activity under the SEBI framework. The net premium impact depends on the strikes chosen, a zero-cost collar is achievable when the premium received from the short call exactly equals the premium paid for the long put.

How It Plays Out

Setup: Manager holds Stock A at ₹2,500. Buys a put at strike ₹2,300, premium ₹70. Sells a call at strike ₹2,700, premium ₹75. Net premium received = ₹5 per share (near zero-cost collar). Lot size 500.

Scenario | Cash Position | Long Put (₹2,300) | Short Call (₹2,700) | Net Impact |

Stock rises to ₹3,000 | Gains ₹500/share | Expires worthless | Loses ₹300/share upside | Capped at ₹200 + ₹5 net premium |

Stock rises to ₹2,700 | Gains ₹200/share | Expires worthless | Expires (keeps premium) | Best outcome: ₹205/share |

Stock stays flat | No change | Expires worthless | Expires (keeps premium) | Small gain from net premium |

Stock falls to ₹2,300 | Loses ₹200/share | At strike (no value as such) | Expires (keeps premium) | Loss floored at ₹195/share* |

Stock falls to ₹1,800 | Loses ₹700/share | Gains ₹500/share | Expires (keeps premium) | Loss floored at ₹195/share* |

*Maximum loss regardless of how far the stock falls = Stock Price − Put Strike − Net Premium = ₹2,500 − ₹2,300 − ₹5 = ₹195/share.

The last row is the collar's defining value. No matter how catastrophically the stock falls, the loss cannot exceed the distance between the current price and the put strike, minus any net premium received. Equally, the first row shows the cost, a sharp rally above the call strike means the manager is capped and watches further gains pass by.

The collar does not eliminate risk. It converts an open-ended risk profile into a bounded one, with both the worst case and the best case clearly defined before the position is even entered.