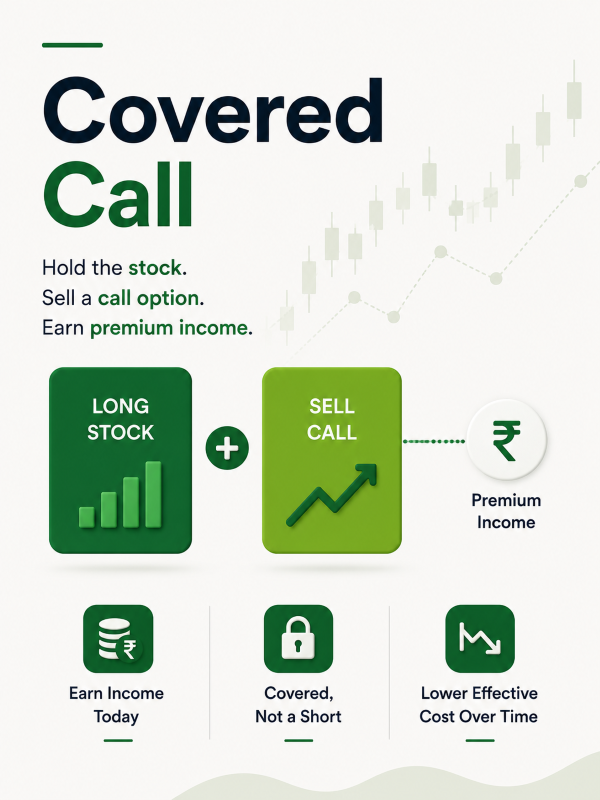

A covered call is a strategy where the manager holds a stock in the portfolio and simultaneously sells a call option on the same stock. The premium collected from selling the call becomes immediate income. In exchange, the manager gives up the right to profit beyond the strike price if the stock rallies sharply.

The word "covered" is important. The manager already owns the stock, so if the call buyer exercises, the manager simply delivers shares already held. There is no naked short exposure. The downside of the stock position remains fully open, partially cushioned only by the premium collected.

When Does an SIF Manager Use This?

A manager uses a covered call when they hold a stock with a positive long-term view but expect it to trade sideways in the near term, perhaps after a strong run-up, or while waiting for the next catalyst. Rather than sitting on a flat position earning nothing, selling a call generates income from that idle period.

It is also used to partially reduce the effective cost of holding a position over time, each premium collected lowers the average acquisition cost of the stock.

In the SIF context, since the manager already holds the underlying stock, the short call is covered and does not represent unhedged short exposure. It therefore does not consume the 25% unhedged short limit. Per the SEBI circular, offsetting is permitted between cash and derivative positions on the same underlying, the covered call sits within this framework as a hedged combination, not a directional short bet.

How It Plays Out

Setup: Manager holds Stock A at ₹2,500. Sells a call option at strike ₹2,700, premium ₹90, lot size 500. Premium collected = ₹45,000 per contract.

Scenario | Cash Position (Long Stock A) | Short Call (Strike ₹2,700) | Net Impact |

Stock rises to ₹3,000 | Gains ₹500/share | Call exercised, must sell at ₹2,700, loses ₹300/share upside | Capped gain: ₹200 + ₹90 premium = ₹290/share |

Stock rises to ₹2,700 | Gains ₹200/share | Call expires (keeps full premium ₹90) | Best outcome: ₹290/share |

Stock stays flat at ₹2,500 | No change | Call expires (keeps full premium ₹90) | Earns ₹90/share from premium alone |

Stock falls to ₹2,200 | Loses ₹300/share | Call expires (keeps premium ₹90) | Net loss ₹210/share (premium provides partial cushion only) |

The second and third rows are where the covered call shines, the stock goes nowhere or rises modestly, the call expires worthless, and the manager pockets the premium. The first row shows the cost of the strategy i.e. a sharp rally above the strike means the manager participates only up to the strike, leaving significant upside on the table. The fourth row is the real risk, the premium cushions a falling stock only partially. A sharp fall still hurts.