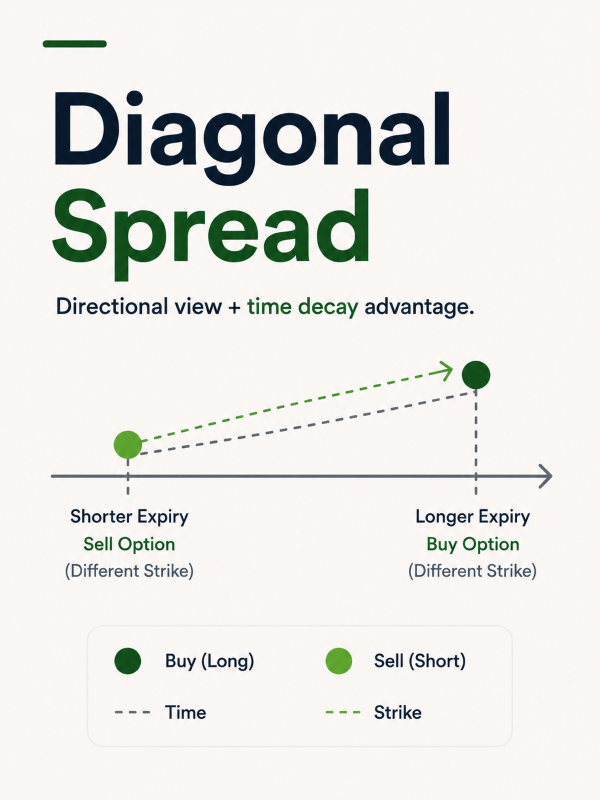

The structure involves buying a longer-dated option at one strike and selling a shorter-dated option at a different strike on the same underlying. Unlike a calendar spread where both options share the same strike, and unlike a vertical spread where both options share the same expiry, a diagonal spread varies both dimensions simultaneously. The result is a strategy that expresses a directional view, like a vertical spread, while also benefiting from time decay on the near-term sold option, like a calendar spread.

Long vs Short

Long Diagonal Spread | Short Diagonal Spread | |

Built by | Buy longer-dated option at favorable strike + Sell shorter-dated option at different strike | Sell longer-dated option + Buy shorter-dated option at different strike |

Profit when | Stock moves toward bought strike while near-term sold option decays | Near-term option moves significantly before expiry |

Loss when | Stock moves sharply against position | Stock stays flat — time decay works against sold longer-dated leg |

Max loss | Net premium paid | Open-ended on the longer-dated sold leg |

The long diagonal spread is the practically relevant and more commonly used version. The short diagonal carries significant open-ended risk on the longer-dated sold leg and is rarely the tool of choice in a regulated SIF portfolio.

When Does an SIF Manager Use This?

A manager uses a long diagonal spread when they have both a directional view on a stock and a time-based view, believing the stock will move gradually toward a target over a longer period while staying relatively quiet in the near term.

The near-term sold call generates time decay income during the quiet period. The longer-dated bought call retains directional exposure to the gradual move toward the target. If the stock stays below the sold call's strike through near-term expiry, the manager keeps the premium collected and still holds the longer-dated directional position, but now at a reduced net cost. The near-term sold option can then be rolled by selling a new short-dated call against the already held longer-dated position, repeatedly reducing the cost of the longer-dated exposure over time.

A bearish diagonal works the same way in reverse, buying a longer-dated put and selling a shorter-dated put at a lower strike for a stock the manager expects to drift lower gradually.

The diagonal spread is also used as an alternative to a covered call when the manager does not hold the underlying stock by replacing the cash position with a longer-dated in-the-money call and selling a shorter-dated out-of-the-money call against it. This replicates much of the covered call's income-generating behavior at a fraction of the capital cost.

In the SIF context, the sold near-term leg counts toward gross exposure at full notional value per the SEBI circular, Market Price of Underlying × Lot Size × Number of Contracts. The bought longer-dated leg is counted on premium paid only. The net exposure is therefore moderate, primarily driven by the sold near-term leg. The directional element of the diagonal, achieved through the longer-dated bought option, adds relatively little to gross exposure given the premium-based calculation.

How It Plays Out

Setup: Stock A trading at ₹2,500. Lot size 500. Bullish long diagonal: buy next-month call at ₹2,500 strike (premium ₹140), sell near-month call at ₹2,700 strike (premium ₹50). Net premium paid = ₹90 per share. Total cost = ₹45,000.

Scenario | Near-Month Short Call (₹2,700 strike, ₹50 premium) | Next-Month Long Call (₹2,500 strike, ₹140 premium) | Net Impact |

Stock stays at ₹2,500 at near-term expiry | Expires worthless, keeps ₹50 | Still holds significant value, retains most of ₹140 | Best near-term outcome, as cost of long call effectively reduced to ₹90 |

Stock rises to ₹2,700 at near-term expiry | At strike, expires | Gains ₹200/share intrinsic value + remaining time value | Strong outcome, directional view playing out |

Stock rises sharply to ₹3,000 at near-term expiry | Loses ₹300/share | Gains ₹500/share intrinsic value | Net gain but short call caps near-term upside |

Stock falls to ₹2,200 at near-term expiry | Expires worthless, keeps ₹50 | Long call loses significant value due to stock moving away from strike | Net loss, premium cushioned but directional bet not working |

Stock gradually rises to ₹2,700 by next-month expiry | Already expired, premium kept | Gains ₹200/share at expiry | Ideal full outcome as the time and direction both correct |

The fifth row is the diagonal's ideal full-cycle outcome where the stock stays quiet in the near term, allowing the sold option to expire worthless, then gradually moves to the target by the longer-dated expiry. Both the time decay capture and the directional gain are realised in sequence.

The third row shows the diagonal's limitation relative to a plain long call, as a sharp near-term move beyond the sold strike means the short leg loses value rapidly, partially offsetting the long leg's gains. The manager participates in the upside but not fully above the sold call's strike until the near-term expiry passes.