Indian equity mutual fund investors have always had a one-way relationship with markets. You invest, markets go up, you make money. But sometimes a fund manager might see a stock as grossly overvalued, fundamentally broken, or headed for a severe correction, but beyond reducing its weight or avoiding it, there was nothing they could do with that bearish conviction.

The Equity Long-Short Fund changes this at a structural level.

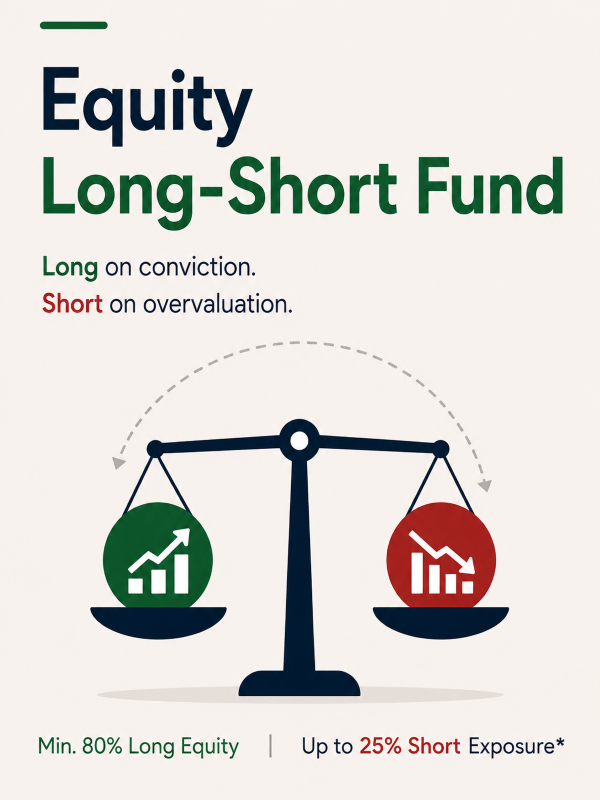

What This Fund Does Differently

The fund maintains a minimum 80% allocation to listed equity and equity-related instruments; this is the core of the portfolio, working exactly as any equity fund does. On top of this, the manager can take unhedged short positions of up to 25% of net assets through exchange-traded equity derivatives i.e. futures and options on stocks and indices.

In a traditional equity fund, a manager's skill is measured only by which stocks they buy. Here, it's measured by both sides: which stocks they go long on and which they short. A manager who correctly identifies an overvalued sector and shorts it while being long on an undervalued one generates returns from both calls. In a falling market, a well-constructed short book can meaningfully reduce drawdowns.

This is not a market-neutral fund. With 80% minimum in long equity, the portfolio still moves largely with equity markets. The 25% short cap ensures it stays fundamentally equity-oriented, with the short book cushions. The shorts are also implemented only through exchange-traded derivatives, promoting transparency, regulation, and margining through clearing corporations.

Where This Strategy Shines

The short book earns when bearish calls play out, making sideways and moderately falling markets genuinely workable, not just survivable. It also shines in stock-specific environments where valuation dispersions are wide, when some stocks are clearly expensive and others clearly cheap, a skilled manager can exploit both ends of that gap simultaneously.

The 25% short cap means in a sharp broad market crash, the cushion is real but limited. The strategy also demands significantly more from the fund manager than a traditional equity fund, as getting both the long and short calls right consistently is harder than getting just one side right. Manager selection matters more here than in almost any other category.