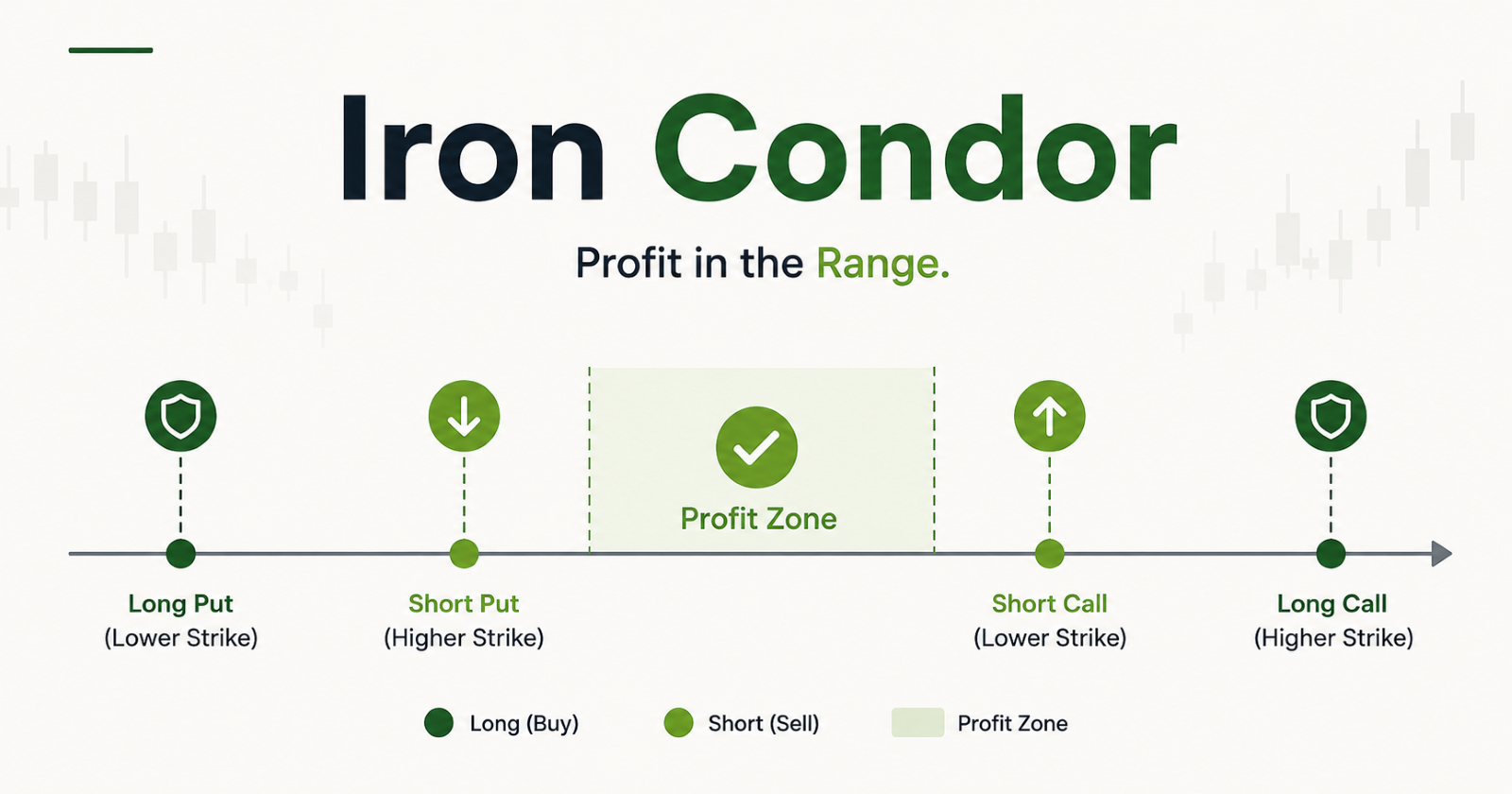

An iron condor is built on one conviction: the stock will stay within a defined price range until expiry. Not bullish. Not bearish.

The structure combines four options at four different strikes (a lower put, a higher put, a lower call, and a higher call), all on the same underlying and same expiry. The manager sells an out-of-the-money put and an out-of-the-money call, collecting premium on both sides, and simultaneously buys a further out-of-the-money put and call to cap the maximum loss. The result is a position that earns the net premium collected as long as the stock stays between the two sold strikes, with fully defined maximum loss beyond either outer strike.

Long vs Short

Long Iron Condor | Short Iron Condor | |

Built by | Buy inner strikes (put and call) + Sell outer strikes (put and call) | Sell inner strikes + Buy outer strikes |

Profit when | Stock breaks out of the inner range | Stock stays within the inner range |

Loss when | Stock stays between inner strikes | Stock breaks beyond inner strikes |

Max gain | Spread width minus net premium paid | Net premium collected |

Max loss | Net premium paid | Spread width minus net premium collected |

When Does an SIF Manager Use This?

Short Iron Condor: Used when the manager expects a stock or index to trade within a defined range through expiry, typically in a low-volatility environment, like after a period of sharp movement that has exhausted itself, or during a known quiet period in the market calendar. By selling an out-of-the-money call and put and buying further out-of-the-money options as protection, the manager collects net premium and keeps it entirely if the stock stays within the sold strikes. The bought outer options mean the maximum loss is always known upfront, unlike a naked short strangle where losses are theoretically unlimited.

Long Iron Condor: Used when the manager expects significant movement but wants defined risk on a volatility bet with a capped maximum gain and capped maximum loss. Less common in SIF strategies but useful when implied volatility is very low, making outer options cheap to buy relative to the inner options sold.

In the SIF context, the iron condor involves two sold options (one call and one put) which per the SEBI circular are each counted at full notional value: Market Price of Underlying × Lot Size × Number of Contracts. The two bought outer options are counted on premium paid only. The bought outer legs do provide a meaningful cap on risk, which is why iron condors are considered more structured and controlled than plain short strangles within a regulated SIF portfolio.

How It Plays Out

Setup: Stock A trading at ₹2,500. Lot size 500. Short iron condor: sell put at ₹2,300 strike (premium ₹55), buy put at ₹2,100 strike (premium ₹25), sell call at ₹2,700 strike (premium ₹60), buy call at ₹2,900 strike (premium ₹30). Net premium collected = ₹55 + ₹60 − ₹25 − ₹30 = ₹60 per share. Total credit = ₹30,000.

Scenario | Short Put (₹2,300) | Long Put (₹2,100) | Short Call (₹2,700) | Long Call (₹2,900) | Net Impact |

Stock stays at ₹2,500 | Expires worthless | Expires worthless | Expires worthless | Expires worthless | Keeps full ₹60/share premium |

Stock rises to ₹2,700 | Expires worthless | Expires worthless | At strike, expires | Expires worthless | Keeps full ₹60/share premium |

Stock rises to ₹2,800 | Expires worthless | Expires worthless | Loses ₹100/share | Expires worthless | Net loss ₹40/share after premium |

Stock rises or above to ₹2,900 | Expires worthless | Expires worthless | Loses ₹200/share | At strike, expires | Maximum loss: ₹200 − ₹60 = ₹140/share |

Stock falls to ₹2,300 | At strike, expires | Expires worthless | Expires worthless | Expires worthless | Keeps full ₹60/share premium |

Stock falls to ₹2,200 | Loses ₹100/share | Expires worthless | Expires worthless | Expires worthless | Net loss ₹40/share after premium |

Stock falls to or beyond ₹2,100 | Loses ₹200/share | At strike, expires | Expires worthless | Expires worthless | Maximum loss: ₹140/share |

The fifth and ninth rows are the iron condor's defining feature, no matter how far the stock moves beyond either outer strike, the loss cannot exceed ₹140 per share. The bought outer options act as hard stops on both sides. Compare this to a short strangle on the same stock: the premium collected would be higher, which is ₹115 per share, but the loss beyond either strike is unlimited. The iron condor sacrifices a part of premium to convert that unlimited risk into a known, bounded worst case of ₹140 per share.