A straddle is a strategy designed for investors who expect a major price move but are uncertain about the direction. Rather than predicting whether a stock will rise or fall, the focus is on the magnitude of the move itself.

The structure is simple: buy or sell both a call and a put on the same underlying, at the same strike price (closest to the current market price of the underlying asset), with the same expiry. The long straddle profits when the stock moves sharply in either direction. The short straddle profits when the stock barely moves at all.

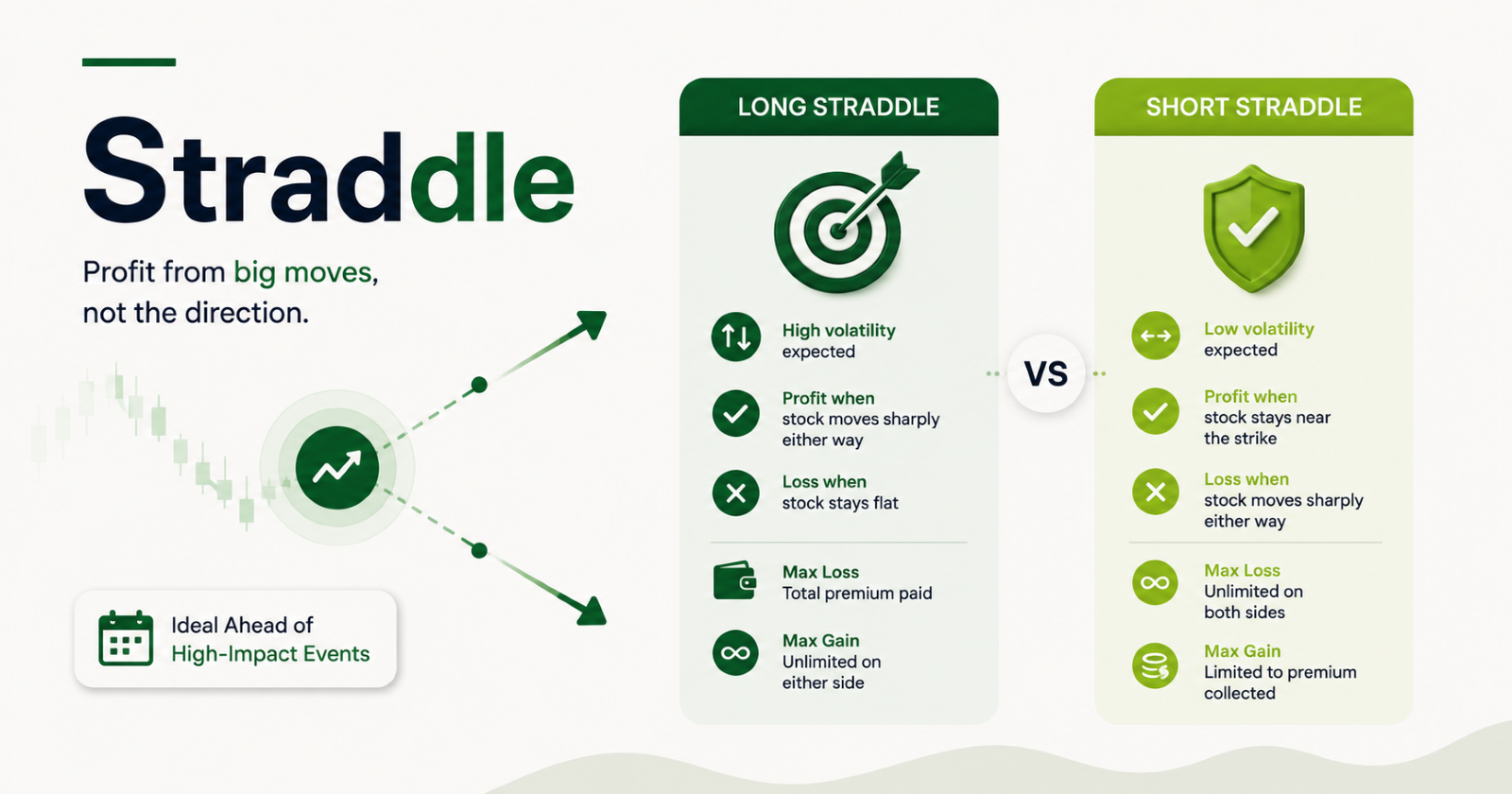

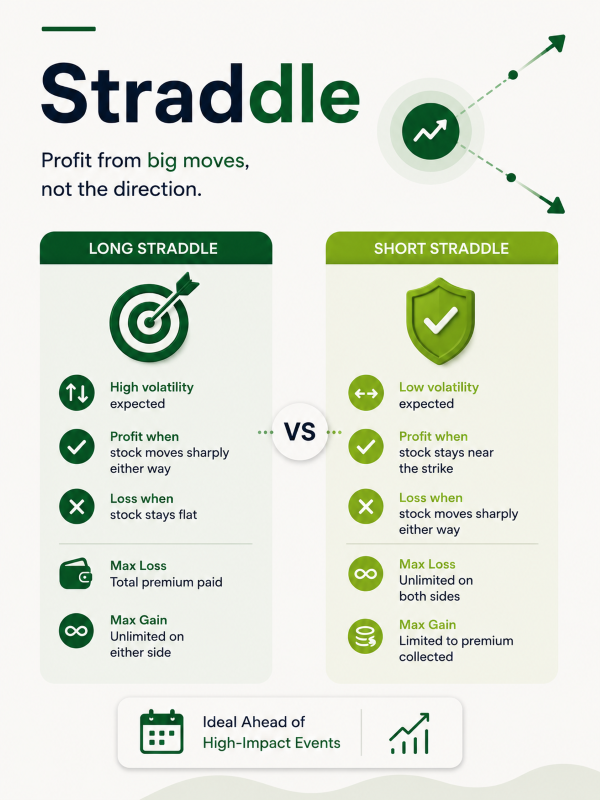

Long vs Short

Long Straddle | Short Straddle | |

View | High volatility expected | Low volatility expected |

Profit when | Stock moves sharply either way | Stock stays near the strike |

Loss when | Stock stays flat | Stock moves sharply either way |

Max loss | Total premium paid | Unlimited on both sides |

Max gain | Unlimited on either side | Limited to premium collected |

When Does an SIF Manager Use This?

Long Straddle is generally used ahead of a high-impact binary event like a major earnings announcement, a court verdict on a company, or a key policy decision, where the outcome is genuinely uncertain but the reaction is expected to be sharp regardless of which way it goes. The manager does not need a directional view. They simply need to be right that the stock will move enough to recover the premium paid on both legs.

Short Straddle, Used when the manager expects a stock to trade in a tight range, perhaps after a period of high volatility that has now settled, or in a stock with predictable, stable earnings. By selling both the call and put, the manager collects premium on both sides. As long as the stock stays near the strike at expiry, both options expire worthless and the full premium is retained.

Per the SEBI circular, exposure for options sold = Market Price of Underlying × Lot Size × Number of Contracts, and since both a call and a put are sold, the gross exposure of a short straddle is counted on both legs separately, making it a heavier consumer of the exposure limits.

How It Plays Out

Setup: Stock A is trading at ₹2,500. Manager buys (long straddle) or sells (short straddle) a call and put both at strike ₹2,500, premium ₹90 (call) + ₹85 (put) = ₹175 total per share, lot size 500. Total premium = ₹87,500 per straddle.

Scenario | Long Straddle | Short Straddle |

Stock rises to ₹2,800 | Call gains ₹300, put expires; net gain ₹125/share (₹300-₹175 paid for premium) | Call loses ₹300, put expires; net loss ₹125/share |

Stock rises to ₹2,675 | Breakeven (₹175 move needed) | Breakeven |

Stock stays at ₹2,500 | Both options expire; loses full ₹175 premium | Both expire; keep the full ₹175 premium |

Stock falls to ₹2,325 | Breakeven | Breakeven |

Stock falls to ₹2,100 | Put gains ₹400, call expires; net gain ₹225/share (₹400-₹175 paid for premium) | Put loses ₹400, call expires; net loss ₹225/share |

The breakeven rows are critical. A long straddle only profits if the stock moves more than the total premium paid in either direction (₹175 as per this example). If the expected big move does not materialise, the entire premium is lost. The short straddle's risk is the mirror of this; any move beyond the premium collected on either side starts generating unlimited losses.