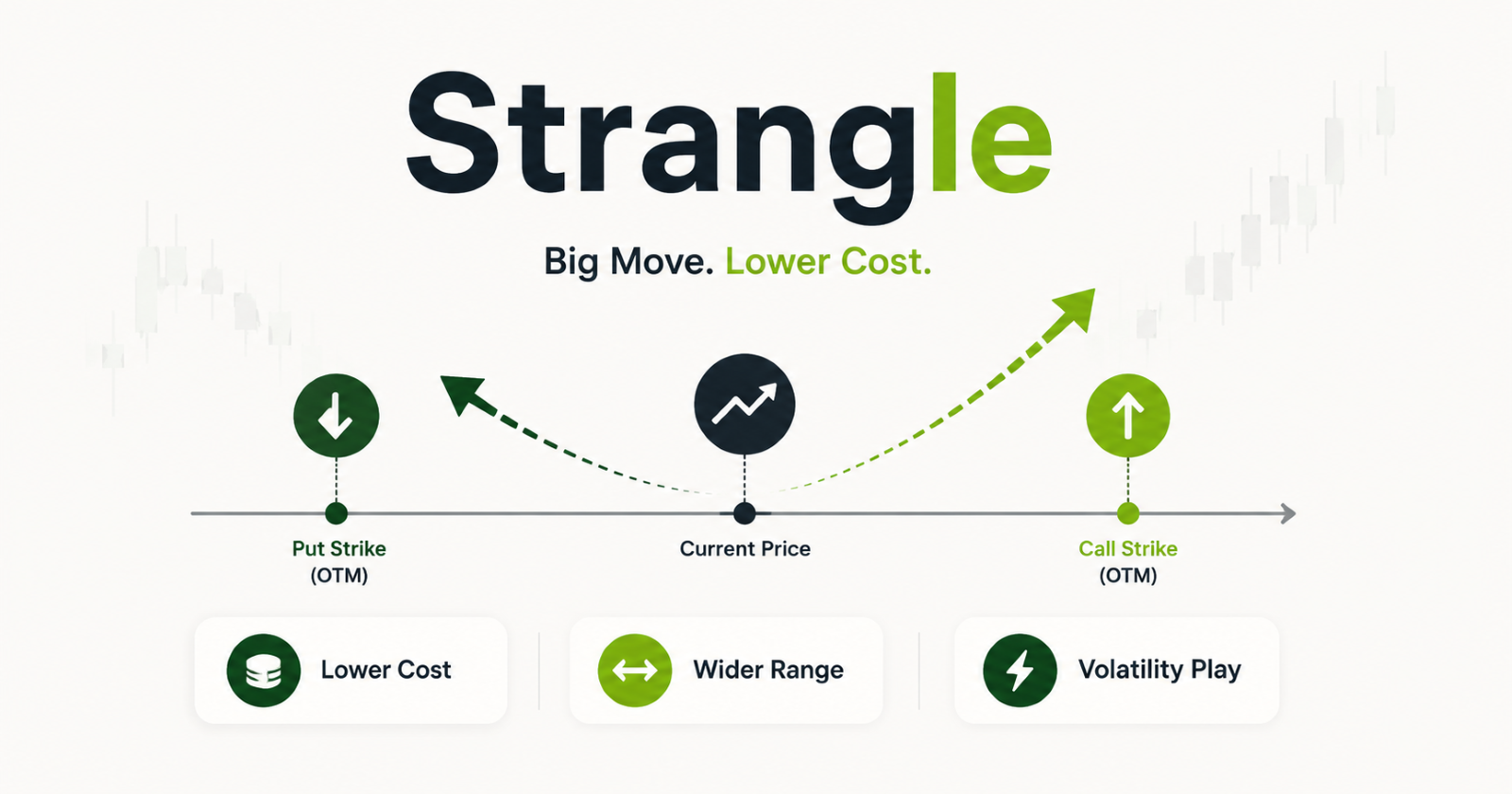

A strangle is a volatility strategy for investors who expect a significant price move but want a lower-cost alternative to a straddle. Instead of buying or selling both options at the same strike price, the strangle uses two different strikes. The call strike is set above the current stock price and the put strike is set below it. Both are out-of-the-money.

This makes the strangle cheaper to buy than a straddle, as out-of-the-money options carry lower premiums than at-the-money ones. The trade-off is that the stock needs to move even further before the position becomes profitable. For the short strangle seller, the wider strikes create a larger "safe zone" where the stock can move without causing a loss.

Long vs Short

Long Strangle | Short Strangle | |

View | Large move expected either way | Stock stays within a range |

Profit when | Stock moves beyond either strike | Stock stays between both strikes |

Loss when | Stock stays between both strikes | Stock breaks beyond either strike |

Max loss | Total premium paid | Unlimited on both sides |

Max gain | Unlimited on either side | Limited to premium collected |

When Does an SIF Manager Use This?

Long Strangle: Used in the same situations as a long straddle, ahead of binary events with uncertain outcomes. The manager chooses a strangle over a straddle when the premium cost of a straddle is too high relative to the expected move. By accepting out-of-the-money strikes, the manager pays less upfront but needs a larger move to profit.

Short Strangle: Used when the manager expects the stock to stay within a defined range, which is the wider than a straddle's single strike allows. By selling an out-of-the-money call and an out-of-the-money put, the manager creates a buffer zone on both sides. As long as the stock stays within that zone at expiry, both options expire worthless and the full premium is kept. The wider strikes make the short strangle more forgiving than a short straddle, but the premium collected is also lower since both options are out-of-the-money.

In the SIF context, as with the short straddle, selling both legs of a strangle carries open-ended risk on both sides. Per the SEBI circular, exposure for options sold = Market Price of Underlying × Lot Size × Number of Contracts, both legs are counted separately, making the short strangle a significant consumer of gross exposure limits. The long strangle, by contrast, is exposure-light since options bought are calculated only on premium paid.

How It Plays Out

Setup: Stock A trading at ₹2,500. Manager buys or sells an out-of-the-money call at strike ₹2,700 (premium ₹60) and an out-of-the-money put at strike ₹2,300 (premium ₹55). Total premium = ₹115 per share, lot size 500. Total cost = ₹57,500 per strangle.

Scenario | Long Strangle | Short Strangle |

Stock rises to ₹3,000 | Call gains ₹300, put expires; net gain ₹185/share (₹300-₹115 paid for premium) | Call loses ₹300, put expires; net loss ₹185/share |

Stock rises to ₹2,815 | Breakeven (₹2,700 + ₹115 premium) | Breakeven |

Stock stays between ₹2,300–₹2,700 | Both expire; loses full ₹115 premium | Both expire; keeps full ₹115 premium |

Stock falls to ₹2,185 | Breakeven (₹2,300 − ₹115 premium) | Breakeven |

Stock falls to ₹1,900 | Put gains ₹400, call expires; net gain ₹285/share (₹400-₹115 paid for premium) | Put loses ₹400, call expires; net loss ₹285/share |

This table shows a volatility bet: the Long buyer pays a ₹115 premium hoping for a massive breakout, while the Short seller pockets that premium hoping the stock stays flat. If the stock explodes past the boundaries (hitting ₹3,000 or ₹1,900), the Long position wins big and the Short position suffers heavy losses. Conversely, if the stock stays trapped quietly between ₹2,300 and ₹2,700, both options expire worthless, meaning the Short seller keeps the full ₹115 profit and the Long buyer loses everything. The positions perfectly offset, breaking even only if the stock moves exactly ₹115 beyond either strike price (at ₹2,815 or ₹2,185).