A put option gives the buyer the right, but not the obligation to sell an underlying asset at a fixed strike price before or on expiry. The buyer pays a premium for this right. The seller collects that premium and takes on the obligation to buy if the buyer exercises.

If a call option is a bet on a stock going up, a put option is its mirror, a tool built around the possibility of a stock going down. In an SIF, managers use puts on both sides. Buying puts to protect against or profit from falling prices. Selling puts to generate income or enter a position at a lower cost.

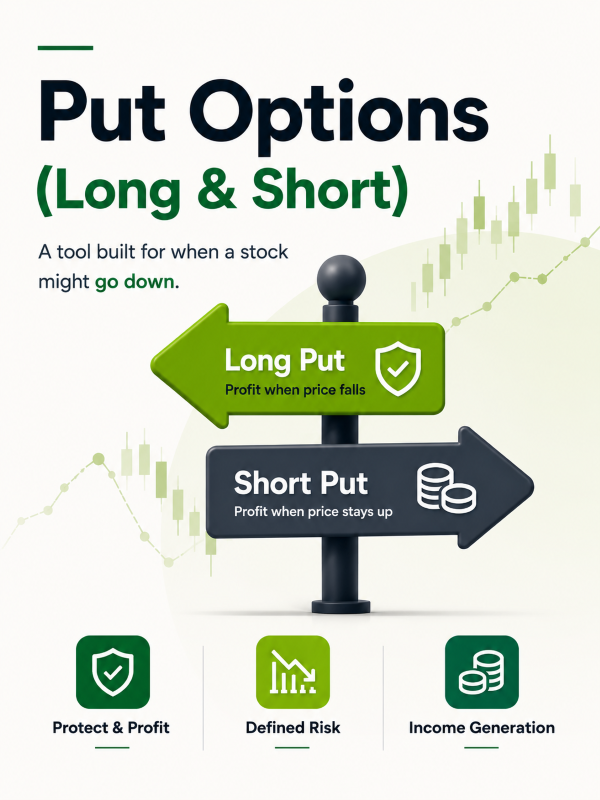

Long vs Short

Long Put | Short Put | |

Profit when | Price falls below strike | Price stays above strike |

Loss when | Price stays above strike | Price falls sharply below strike |

Max loss | Premium paid | Substantial (strike minus zero) |

Max gain | Strike price minus zero (price falls to zero) | Limited to premium collected |

When Does an SIF Manager Use This?

Long Put: When the manager expects a stock or index to fall and wants to profit from that decline with limited risk. Unlike short futures, where losses are unlimited if the stock rises, while a long put caps the downside at the premium paid. This makes it a cleaner bearish tool when the manager wants to limit the cost of being wrong.

Long puts are also used defensively i.e. to protect an existing long position in the portfolio from a potential sharp fall. In that context it becomes a Protective Put.

Per the SEBI circular, exposure for options bought = Option Premium Paid × Lot Size × Number of Contracts. The low exposure calculation makes long puts an efficient hedging instrument within the overall gross exposure limit.

Short Put: When the manager is neutral to bullish on a stock and is comfortable buying it at a lower price. By selling a put at a strike below the current price, the manager collects premium. If the stock stays above the strike, the premium is kept. If it falls below, the manager is obligated to buy the stock at the strike, which is acceptable if the view is that the stock is worth owning at that price.

Per the SEBI circular, exposure for options sold = Market Price of Underlying × Lot Size × Number of Contracts.

How It Plays Out

Setup: Manager buys a put on Stock A at strike ₹2,500, premium ₹85, lot size 500. Separately, sells a put on Stock B at strike ₹900, premium ₹50, lot size 400.

Scenario | Long Put (Stock A) | Short Put (Stock B) |

Price falls sharply | Gains significantly below strike | Loses (must buy at ₹900) |

Price stays flat | Loses premium (₹42,500) | Keeps full premium (₹20,000) |

Price rises | Only loses premium | Keeps full premium |

The contrast in the first row is the critical one. A sharp fall is the best outcome for the long put buyer and the worst outcome for the short put seller. That asymmetry is precisely why short puts in SIF consume more gross exposure than long puts.