Most debt investors think about credit risk in terms of ratings: AAA is safe, AA is mostly safe, A and below needs caution. What they rarely get to act on is a view about an entire sector's creditworthiness shifting. A real estate sector under stress, an NBFC segment with rising non-performing assets, and a telecom sector carrying unsustainable debt loads. Traditional debt funds might miss the sector-specific bets, but this strategy can.

What This Fund Does Differently

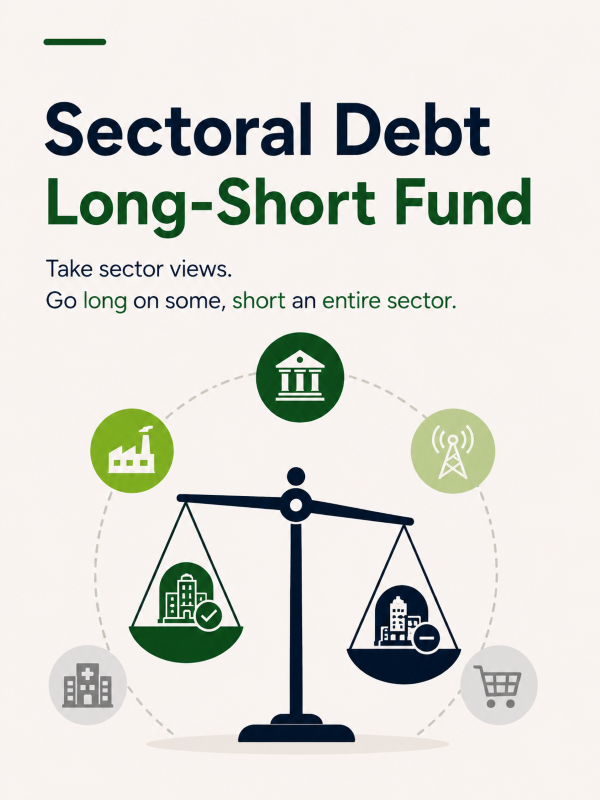

The fund invests in debt instruments of at least two sectors, with a cap of 75% in any single sector. The short exposure follows the same sector-level rule seen in the equity counterpart: up to 25% of net assets can be shorted via debt derivatives, applied across the entire sector.

The sector-wide short rule is critical here. If the manager is bearish on the real estate sector's debt, every real estate debt instrument in the portfolio must be held as a short. No selective hedging, no partial positioning.

Where This Strategy Shines

Equity analysts spend critical time on sector-level research. Debt analysts, have historically focused on individual issuer creditworthiness, i.e., the specific company's balance sheet, cash flows, and repayment capacity.

What this strategy demands is a hybrid skill: understanding both the macro sectoral credit environment and the individual instruments within it. Which sectors are entering a credit stress cycle? Which are emerging from one with improving fundamentals and tightening spreads? A manager who can answer these questions with conviction and act on both the long and short side has a genuinely differentiated performance.

The 75% single-sector cap provides a floor of diversification, but this remains a high-conviction, relatively concentrated credit strategy. The short book can cushion losses when bearish calls are right, but if the long book encounters unexpected credit events, like a sudden rating downgrade, a default, then the damage can be meaningful.