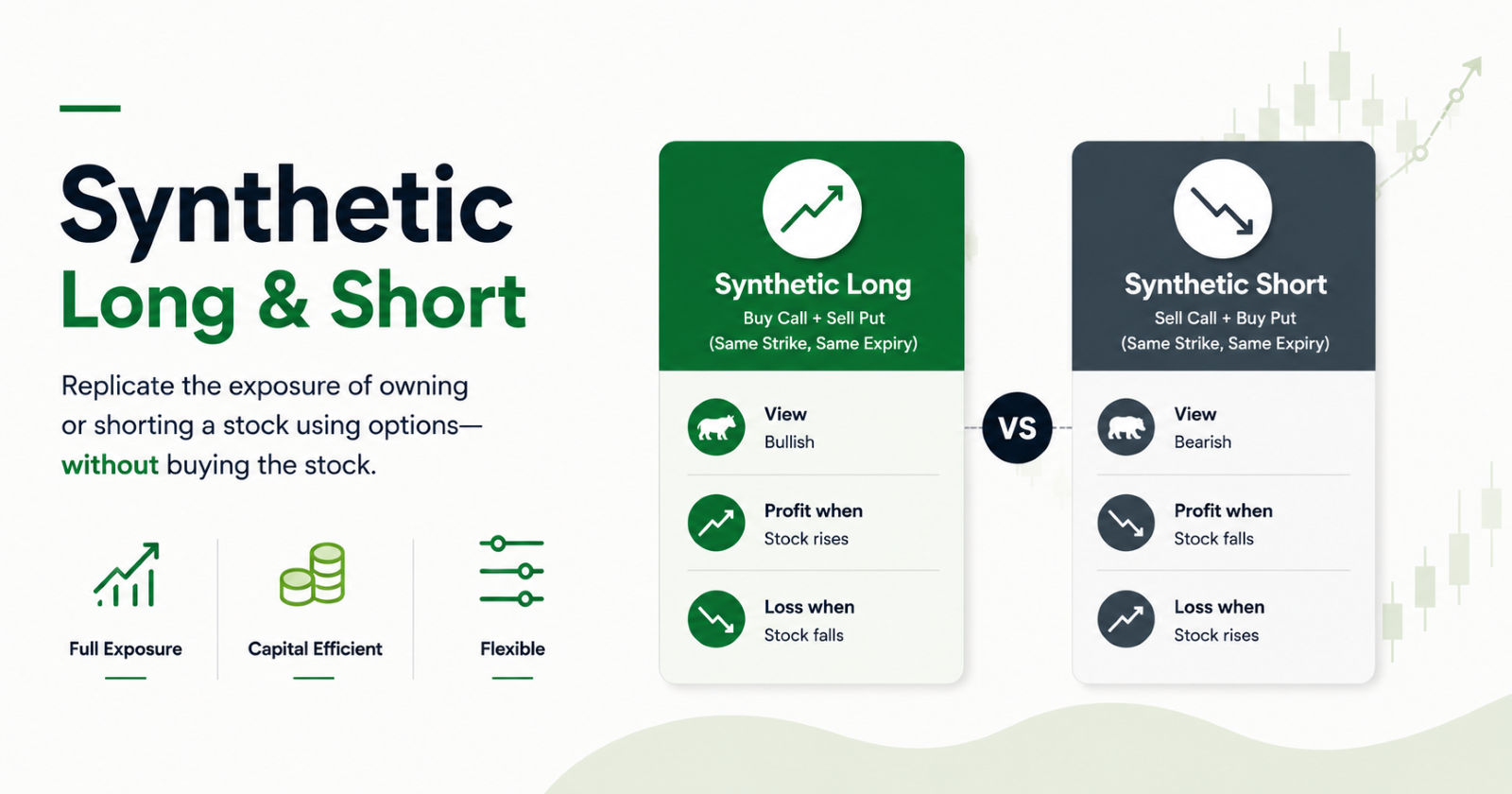

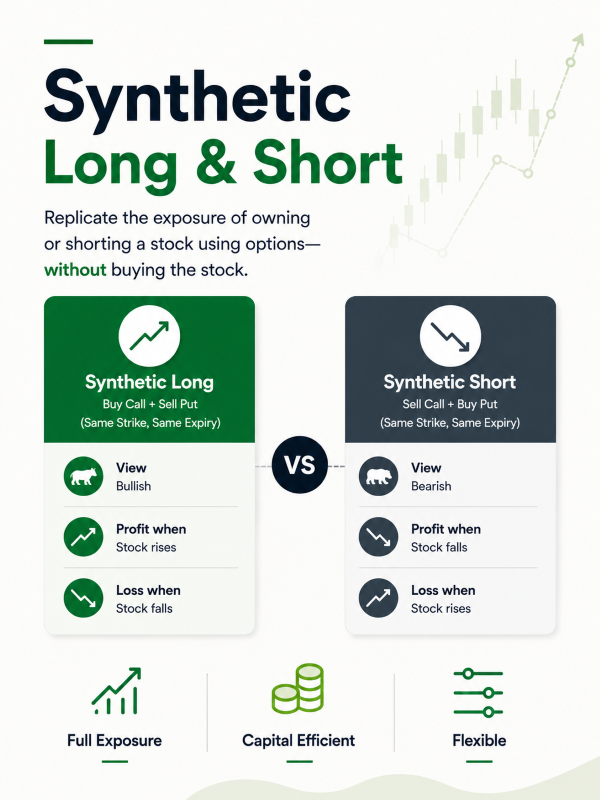

Buying a stock requires full capital upfront. Shorting a stock requires borrowing it, which in India's cash market is restricted and complex. Synthetic positions solve both problems by replicating the economic exposure of owning or shorting a stock entirely through options, without touching the stock itself.

A Synthetic Long replicates owning a stock by buying a call and selling a put at the same strike and expiry, and vice-versa. The position behaves almost identically to holding the actual stock, which gains when the stock rises and loses when it falls, but requires only the net premium as upfront cost rather than the full stock price.

Long vs Short

Synthetic Long | Synthetic Short | |

Built by | Buy Call + Sell Put (same strike, same expiry) | Sell Call + Buy Put (same strike, same expiry) |

Profit when | Stock rises | Stock falls |

Loss when | Stock falls | Stock rises |

Max loss | Substantial, stock falling to zero | Substantial, stock rising without limit |

When Does an SIF Manager Use This?

Synthetic Long: Used when the manager wants full upside exposure to a stock but prefers not to deploy the full capital of buying it outright, keeping that capital available for other positions.

In the SIF context, a synthetic long is particularly useful for managing the gross exposure budget efficiently. Since the bought call is counted on premium paid, and the sold put is counted on the full notional value, the combined exposure of a synthetic long is generally lower than holding the equivalent cash position in the stock.

Synthetic Short: Used when the manager wants to short a stock but finds that futures on that particular stock have poor liquidity or wide bid-ask spreads. By combining a sold call and a bought put at the same strike, the manager achieves the same economic outcome as a short futures position.

This is particularly relevant in the SIF's Equity Ex-Top 100 Long-Short Fund, where short exposure targets non-large-cap stocks. Many mid and small-cap stocks have limited futures liquidity, making synthetic shorts via options a more practical route to expressing a bearish view on those names.

The short leg of a synthetic short counts toward the 25% unhedged short exposure limit under the SIF framework per the SEBI circular. The bought put counts on premium paid only, making its exposure footprint minimal.

How It Plays Out

Setup: Stock A trading at ₹2,500. Lot size 500.

Synthetic Long: Buy call at ₹2,500 strike (premium ₹120), sell put at ₹2,500 strike (premium ₹115). Net premium paid = ₹5 per share.

Synthetic Short: Sell call at ₹2,500 strike (premium ₹120), buy put at ₹2,500 strike (premium ₹115). Net premium received = ₹5 per share.

Scenario | Synthetic Long | Synthetic Short |

Stock rises to ₹2,800 | Gains ₹300/share (call profits, put expires) | Loses ₹300/share (call exercised, put expires) |

Stock stays at ₹2,500 | Near breakeven | Near breakeven |

Stock falls to ₹2,200 | Loses ₹300/share (put exercised, call expires) | Gains ₹300/share (put profits, call expires) |

The near-identical payoff to owning or shorting the actual stock is the defining feature. The only difference is the small net premium at entry, which is the cost or credit of constructing the synthetic rather than transacting in the cash market.