Category: Derivative Strategies

Derivative Strategies

Showing all articles under Derivative Strategies.

Offsetting and Netting in Derivatives

Offsetting nets opposite positions on the same underlying to calculate true exposure, preventing double-counting of risk. SEBI permits offsetting between cash and derivative positions or between two derivative positions on the same underlying with the same expiry.

Sector-Level Shorting: Profiting from Sector Declines

Sector-level shorting lets SIF managers profit from declines across an entire industry using index futures or options. This explains when to use it, how it counts toward the 25% unhedged short limit, and how it interacts with long positions, including a detailed scenario with auto sector stocks.

Mastering the Art of Derivative Pair Trading

Pair trading neutralizes market direction by going long on an outperforming stock and short on a weaker peer, profiting from relative performance. SIF managers use it to express stock-specific views while hedging sector risk.

Diagonal Spread: Balancing Time Decay and Directional Bias

A diagonal spread combines a longer-dated option at one strike with a shorter-dated option at a different strike on the same underlying. This strategy expresses a directional view while benefiting from time decay on the near-term sold leg. Long diagonal spreads are commonly used by SIF managers when they expect gradual stock movement and near-term

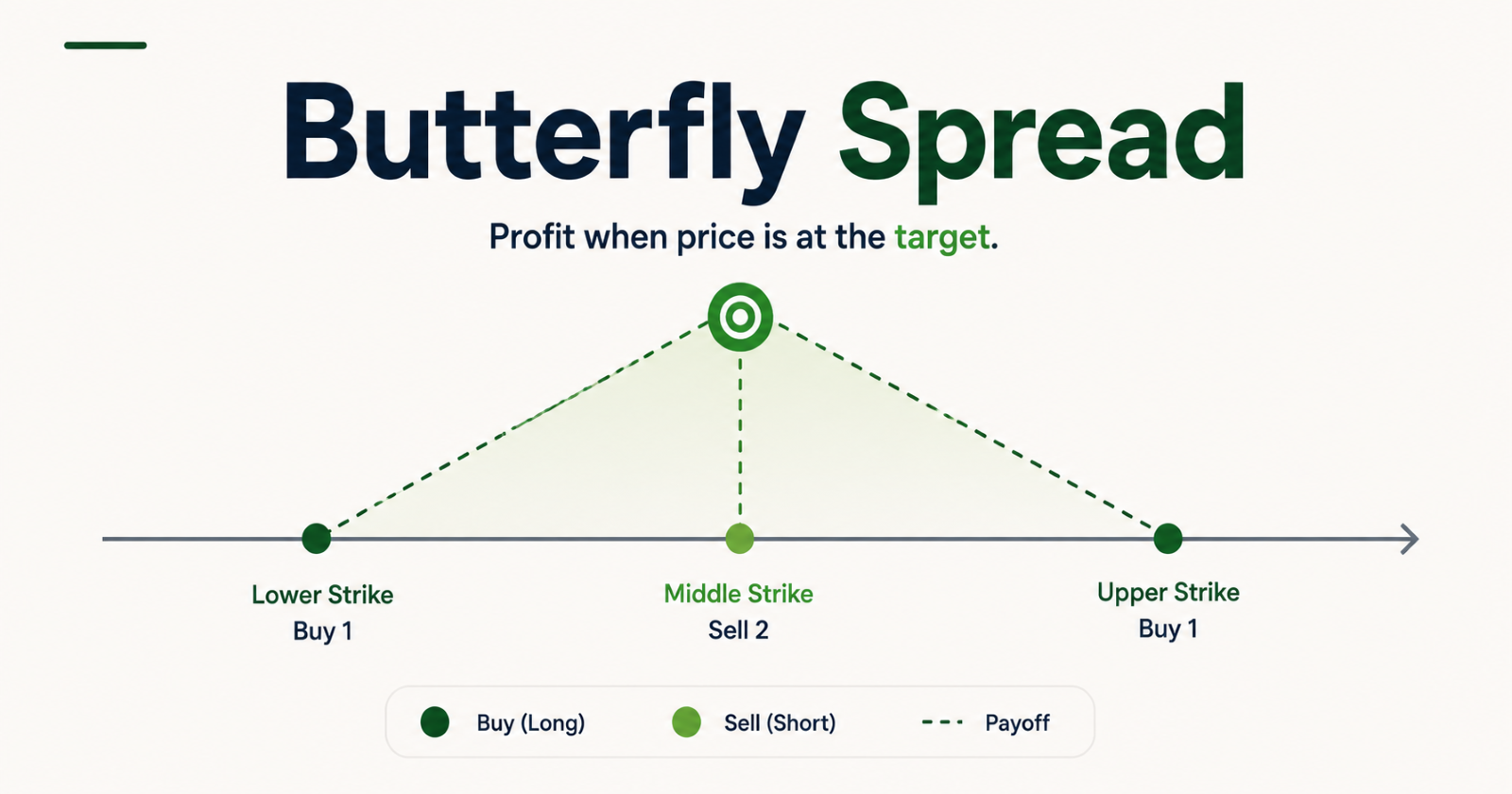

Range-Bound Markets: How to Trade the Butterfly Spread

Learn how to trade the butterfly spread, a low-cost options strategy for range-bound markets. This guide covers construction using three strikes, long vs short butterflies, profit/loss scenarios, and when to use them around earnings or high volatility. Perfect for SIF managers seeking precise price target strategies.

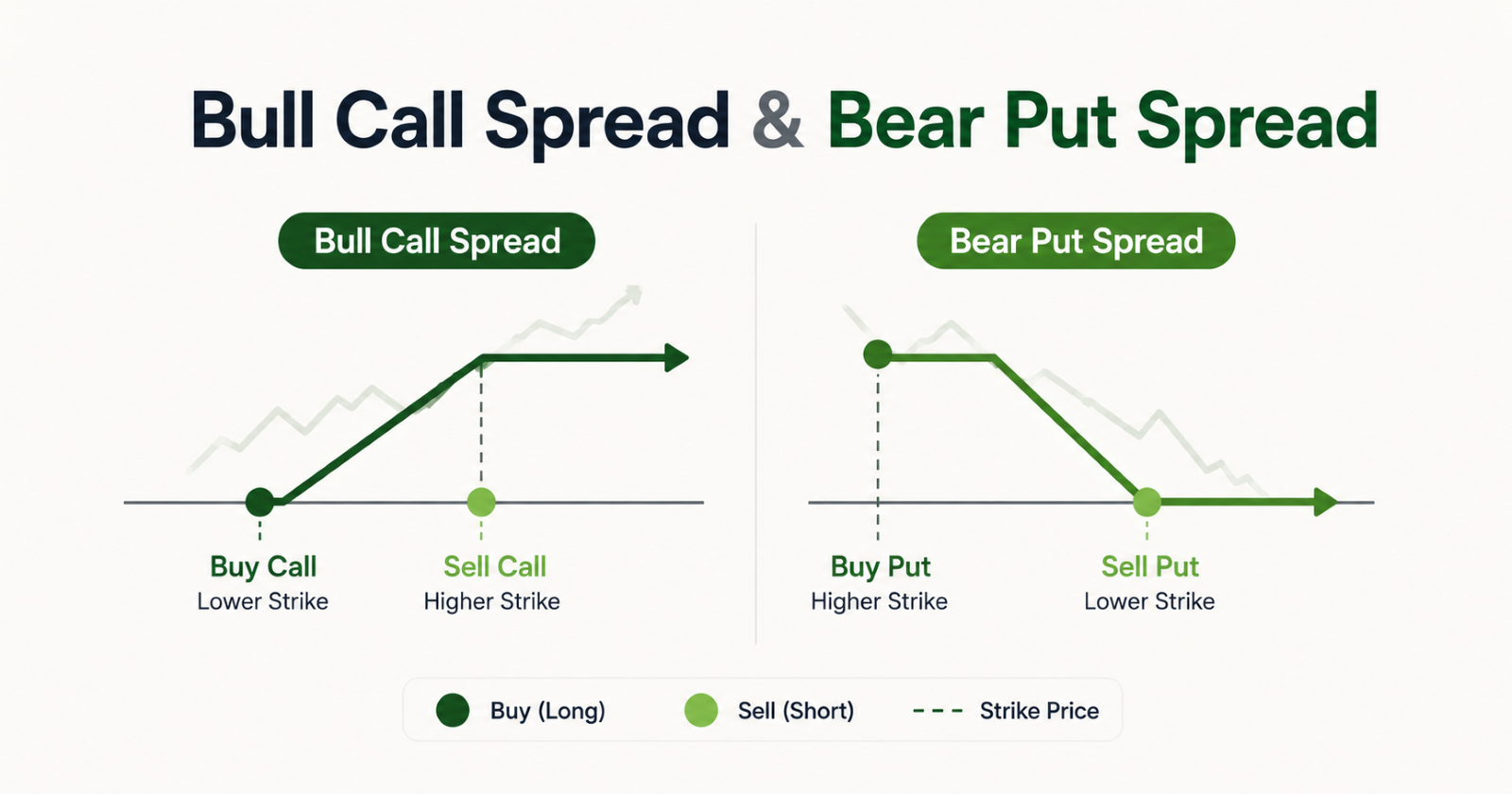

Bull Call Spread & Bear Put Spread

Learn how SIF managers use bull call spread and bear put spread to express moderate directional views with capital efficiency. These option spreads combine buying and selling options at different strikes to reduce cost and cap gains. Understand the risk/reward, SEBI exposure rules, and how they fit within the 100% gross exposure limit.

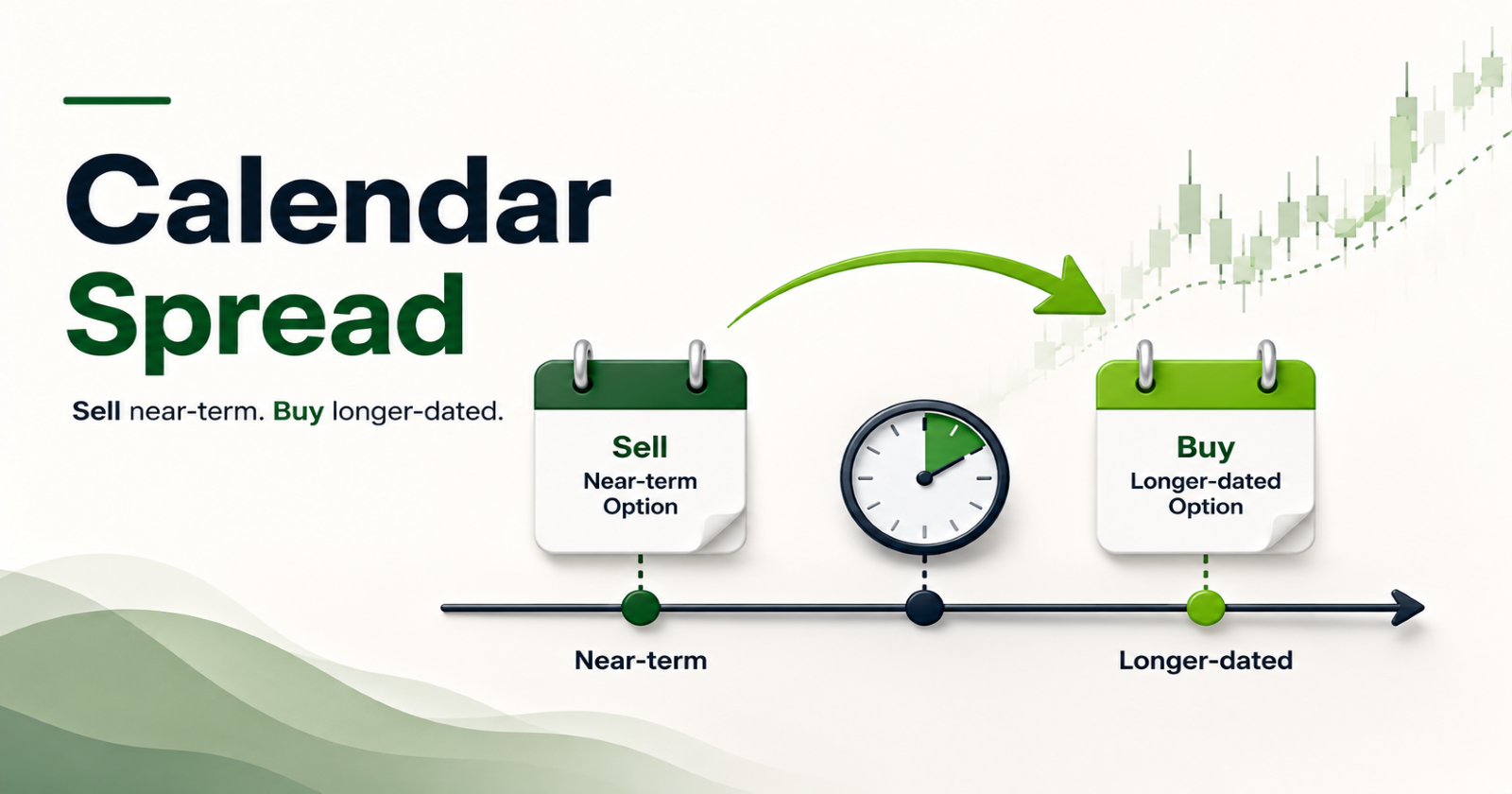

Mastering the Calendar Spread: Volatility, Time Decay, & The Edge

Learn how the calendar spread capitalizes on time decay: sell a near-term option and buy a longer-dated option at the same strike. Ideal for expecting stability near-term and a catalyst later. Covers SIF exposure calculation per SEBI rules.

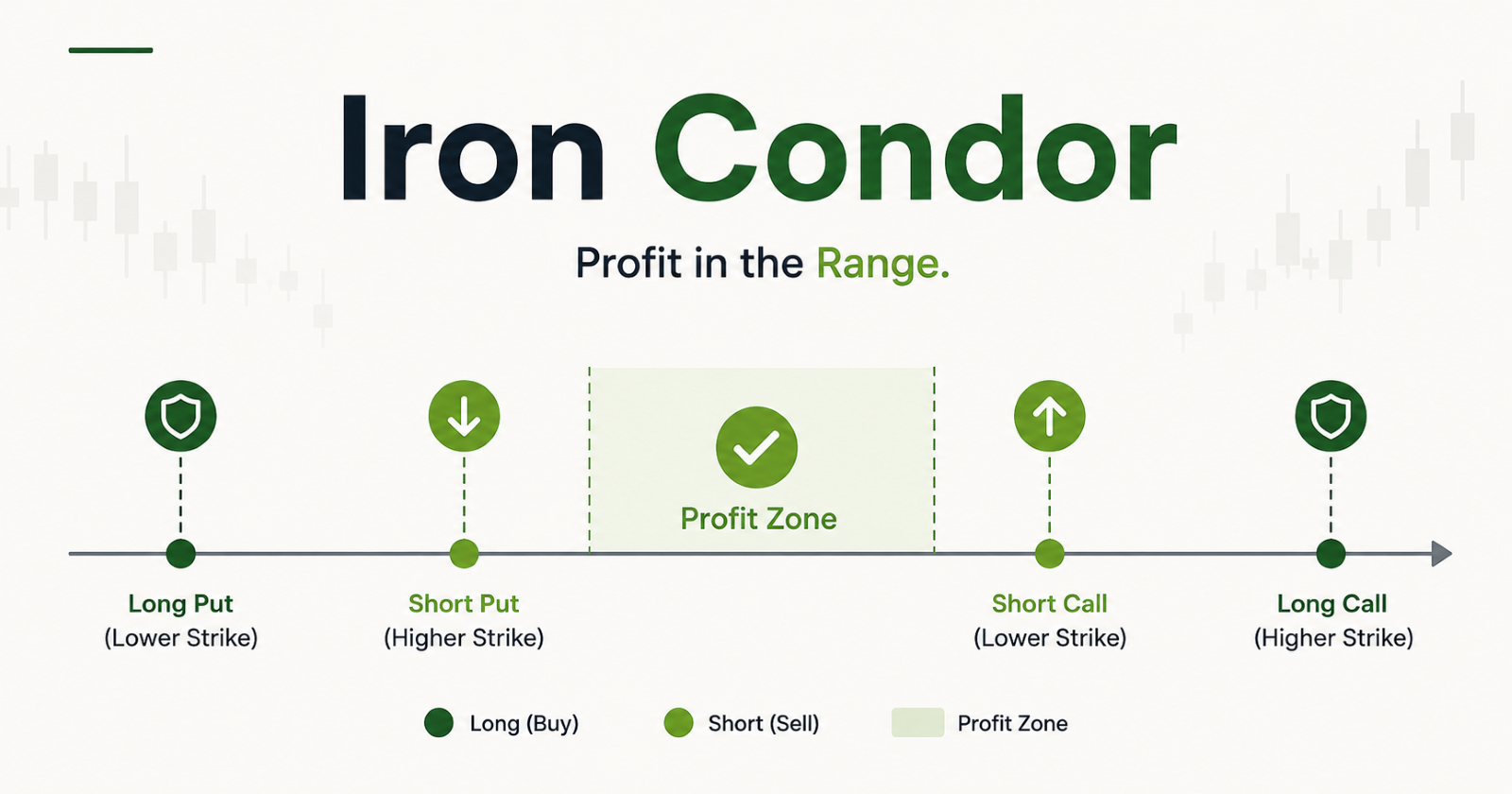

Iron Condor: Defined-Risk Income in a Range-Bound Market

An iron condor combines four options to profit from a stock staying within a range. Learn its construction, long vs short variants, when SIF managers deploy it, SEBI notional value counting rules, and a detailed payoff example.

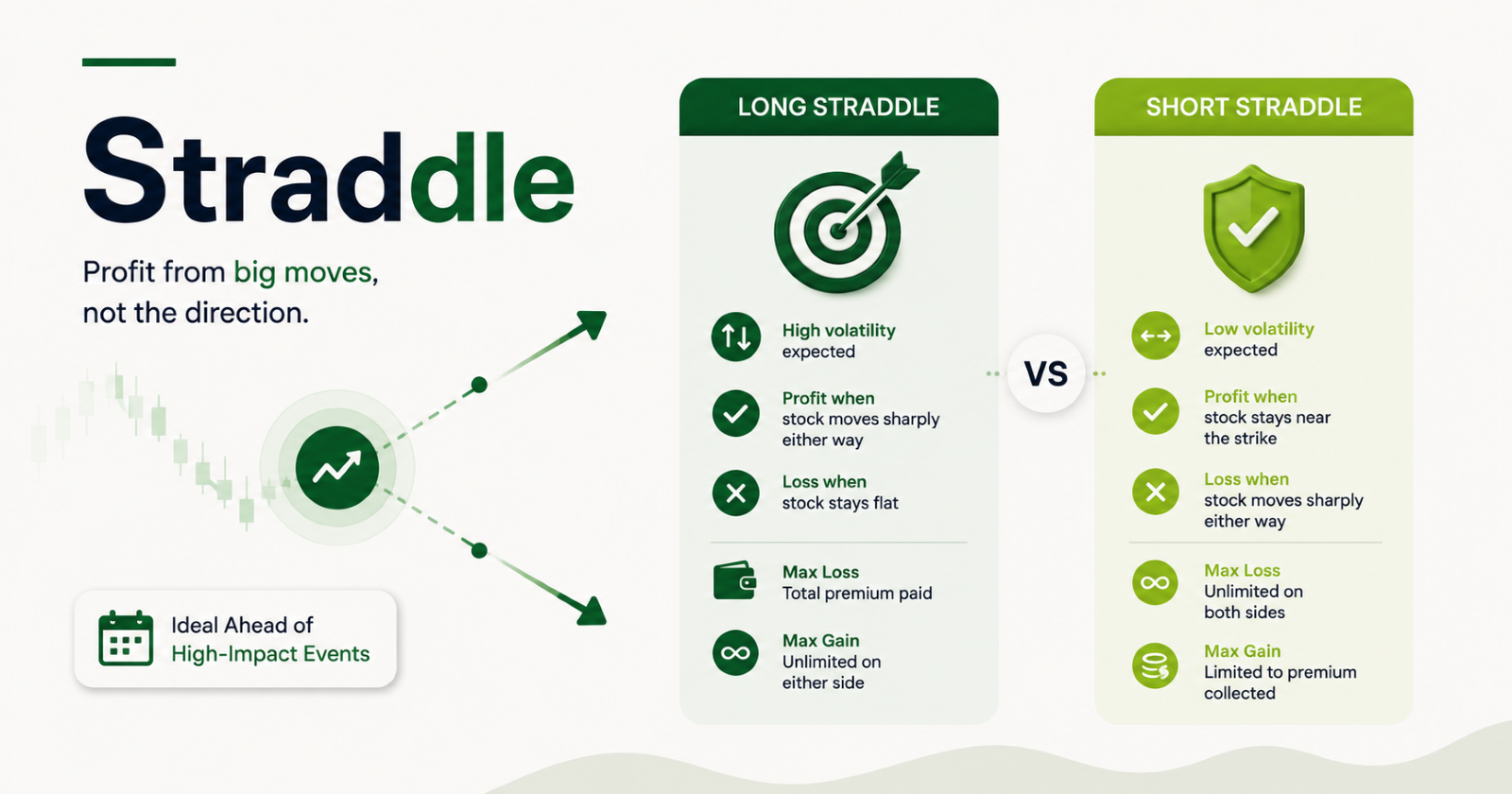

Long vs Short Straddle

This article explains the straddle strategy for Indian SIF managers, covering long and short straddles. It details when to use each: long straddle for high-volatility events like earnings, short straddle for stable markets. Includes profit/loss scenarios, breakeven points, and SEBI exposure limit implications. Perfect for understanding

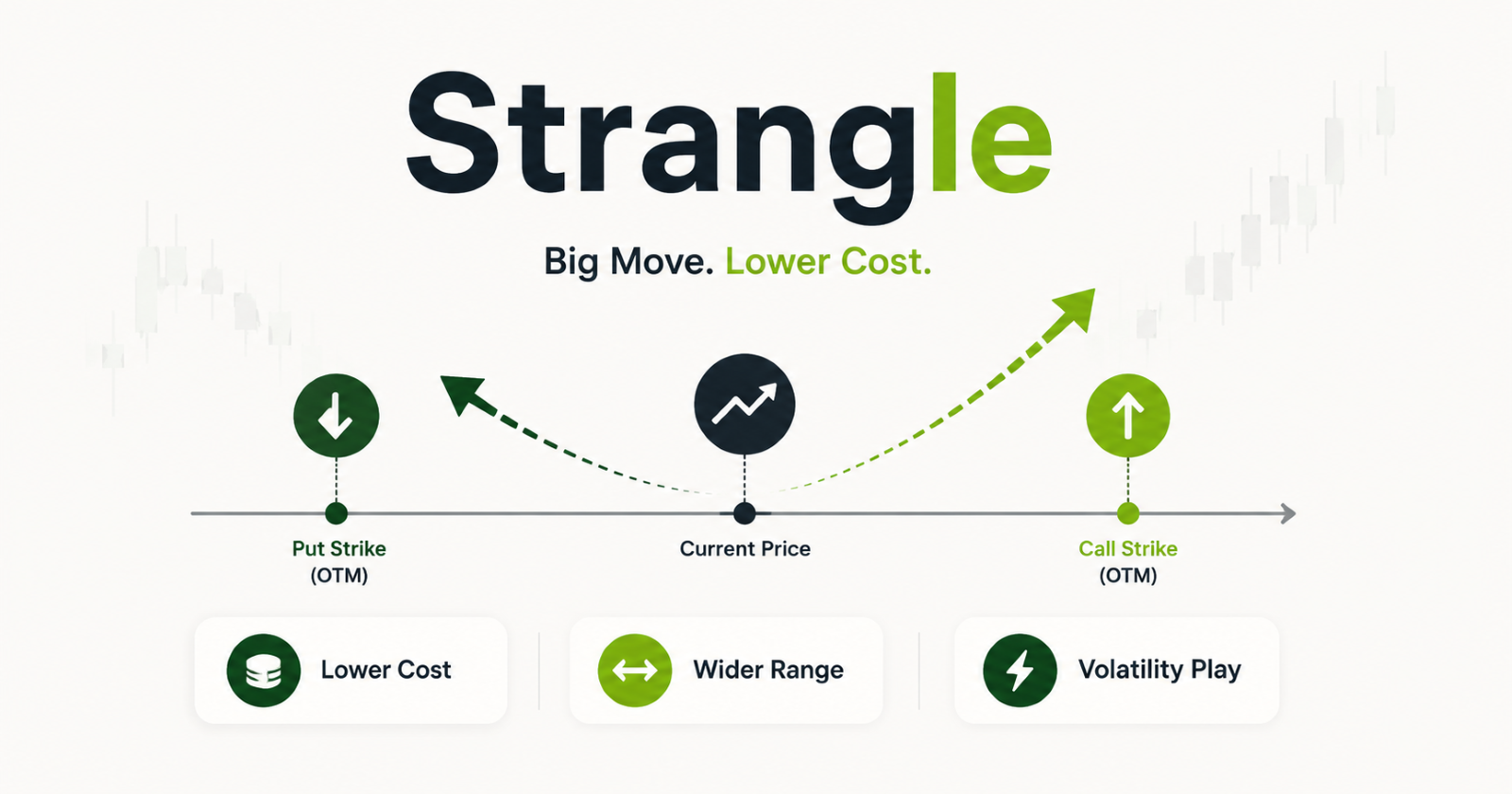

Long vs Short Strangle

A strangle is a lower-cost option strategy than a straddle, using out-of-the-money call and put strikes. Learn the differences between long and short strangles: profit/loss profiles, breakeven points, max gain/loss, and when SIF managers use each. Understand how short strangles consume gross exposure limits under SEBI norms.

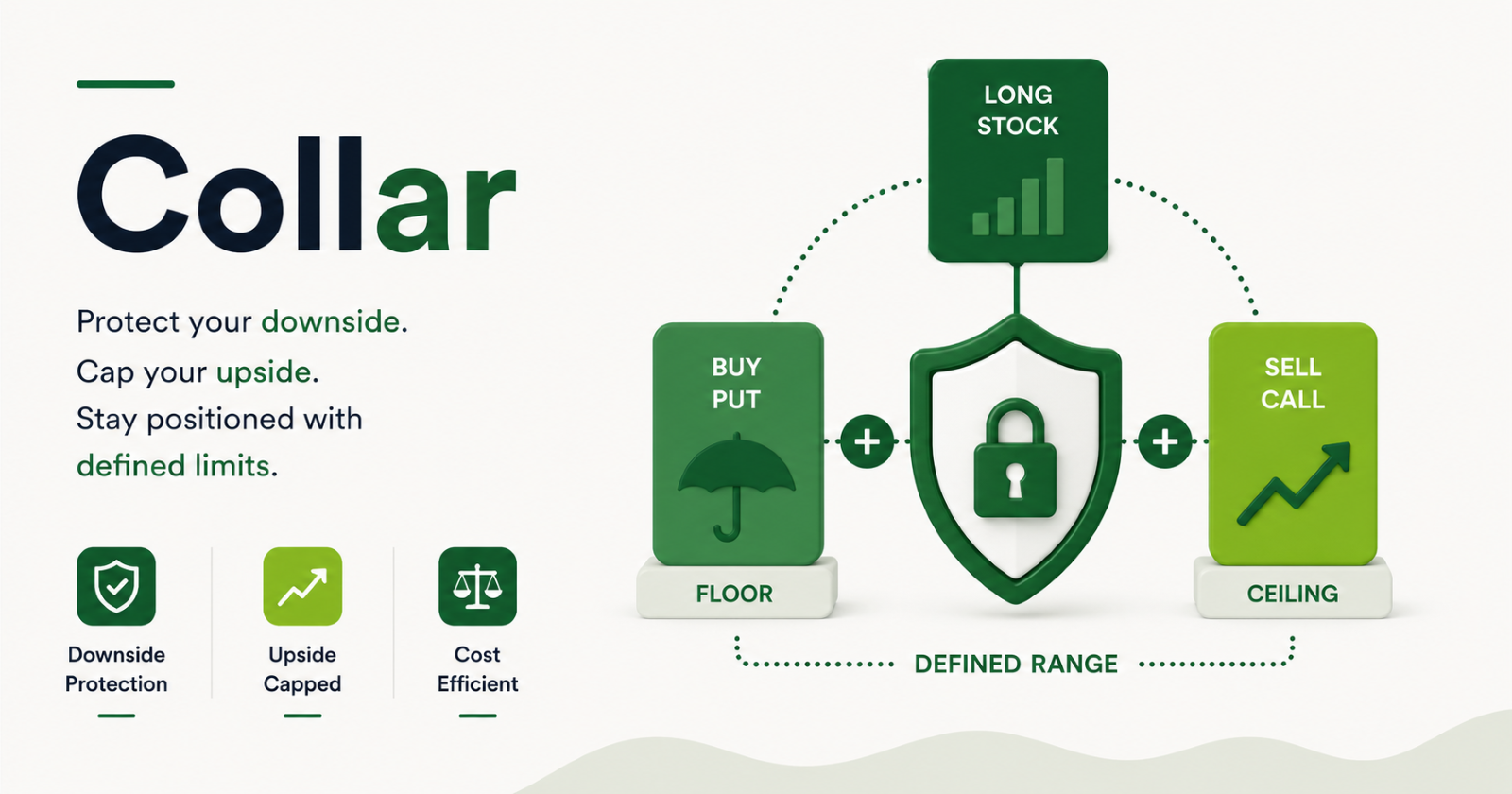

Collar Strategy: Balancing Risk and Reward in Volatile Markets

The collar strategy in SIF combines a protective put and a covered call to cap downside while sacrificing upside. Managers use it when holding stocks through uncertainty, with the short call funding the put. Under SEBI, it qualifies as hedging, not using the 25% unhedged short limit. The result is a bounded risk profile with defined worst-case and

Generating Cash Flow with Covered Calls

A covered call is an options strategy where an SIF manager holds a stock and sells a call option on it to generate immediate premium income, suitable for sideways or modestly rising markets. The manager caps upside but gains premium, partially cushioning downside. This strategy is compliant with SEBI rules as a hedged combination.

How to Use Protective Puts to Limit Downside Risk

A protective put is an options strategy used by SIF managers to hedge downside risk while keeping upside open. By buying a put on a held stock, the loss is capped at a known amount (stock price - strike price + premium) regardless of how far it falls. The cost is just the premium paid. Ideal for near-term uncertainty.

Management of risk with Future Hedge Derivatives

A futures hedge allows SIF managers to protect long stock positions during short-term turbulence without selling. By shorting futures on the same underlying, the hedge neutralises price risk. SEBI permits this hedging without counting toward the 25% unhedged short limit, and netting between cash and derivative positions reduces gross exposure.

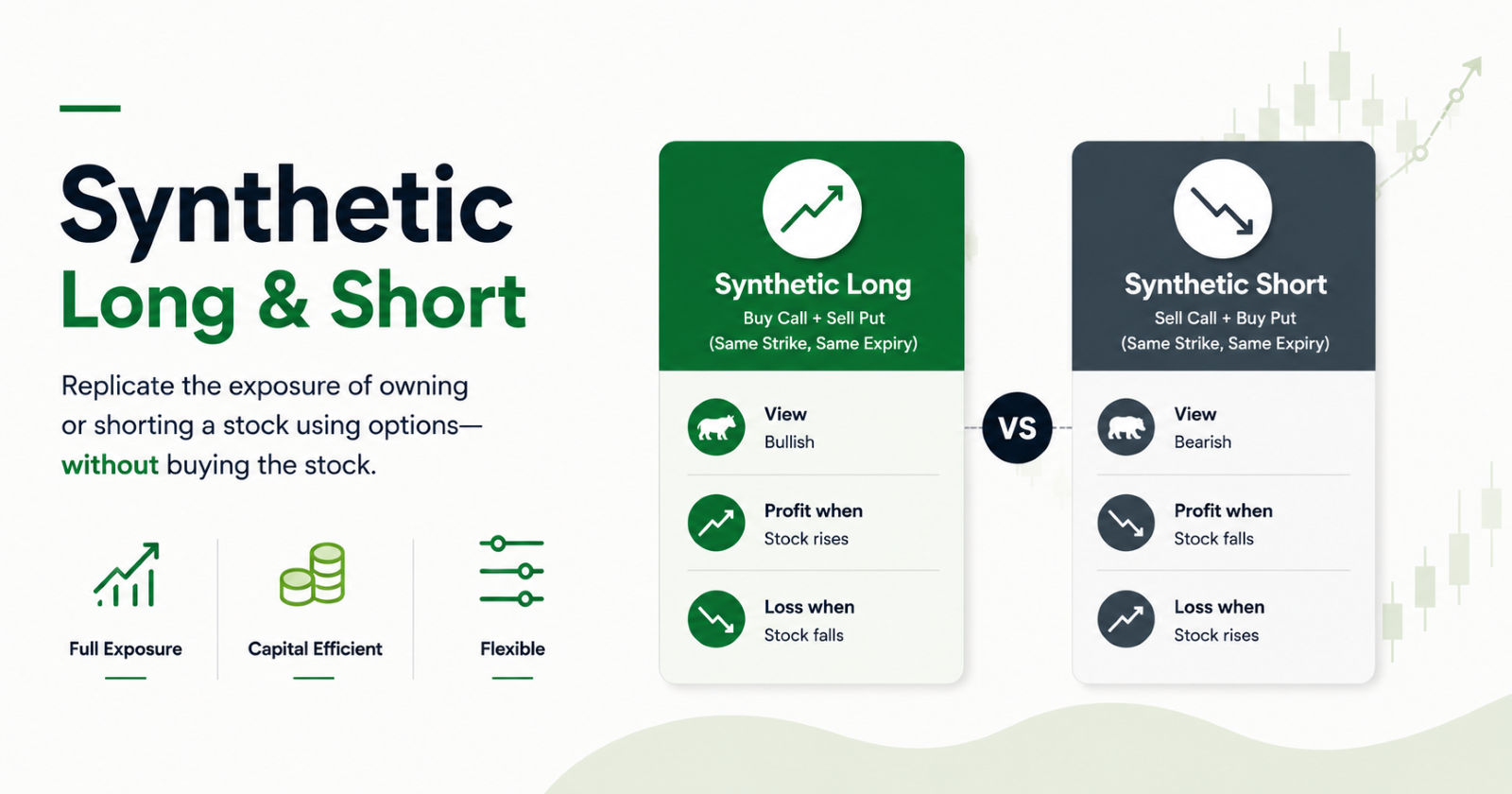

Guide to Synthetic Long and Short Derivative Strategies

Synthetic positions (long & short) replicate stock exposure using options, without owning or borrowing shares. SIF managers use synthetics to reduce capital needed for long positions and to short illiquid mid/small-cap stocks. This article explains construction, payoff, and real SIF use cases with an example.

Futures (Long & Short)

Futures contracts allow SIF managers to gain market exposure or hedge risks without immediate capital deployment. This article explains how Specialised Investment Funds (SIFs) leverage both long and short futures positions, distinguishing their approach from traditional mutual funds. Understand SEBI regulations on derivatives exposure and see